Assets under Construction (AuC) are a special form of tangible assets. They are usually displayed as a separate balance sheet item, requiring separate account determination and their own asset classes. During the construction phase of an asset, all actual postings are assigned to the AuC. Once the asset is completed, a transfer is made to the final fixed asset.

Internal orders are used to capture the costs of AuC during the construction phase. Once the AuC is completed, the final asset is created in the appropriate asset class, and the internal order is set to complete. The next settlement transfers the AuC asset value to the completed asset.

Asset Under Construction Process:

| Asset Acquisition for Constructed Assets (External Procurment) |

| · Create Assets |

| · Posting the Closing Invoice |

| · Define Distribution Rules for Asset Under Construction |

| · Settle Asset under Construction |

| Asset Acquisition for Constructed Asset (Investment Orders) |

| · Creating Investment Order |

| · Releasing Investment Order |

| · Accounts Payable – Posting Invoice to Investment Order |

| · Monitoring Order Progress |

| · Asset under Construction Settlement (collective processing) |

| · Creating Assets for Complete AuC Settlement |

| · Maintaining Settlement Rule for Final Settlement |

| · Final Settlement of the Investment Order (Collective Processing) |

| · Completion of Investment Order |

-

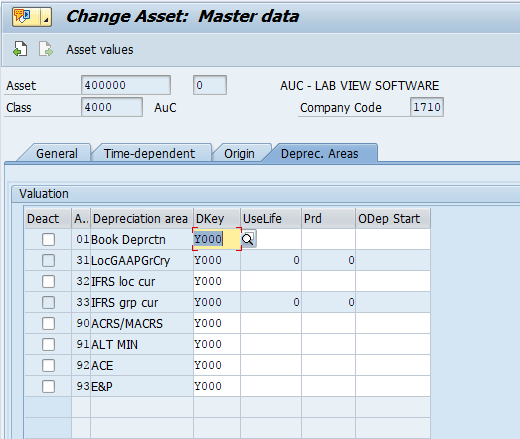

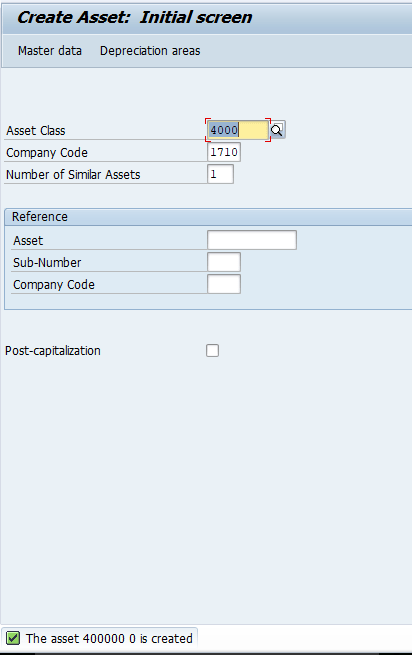

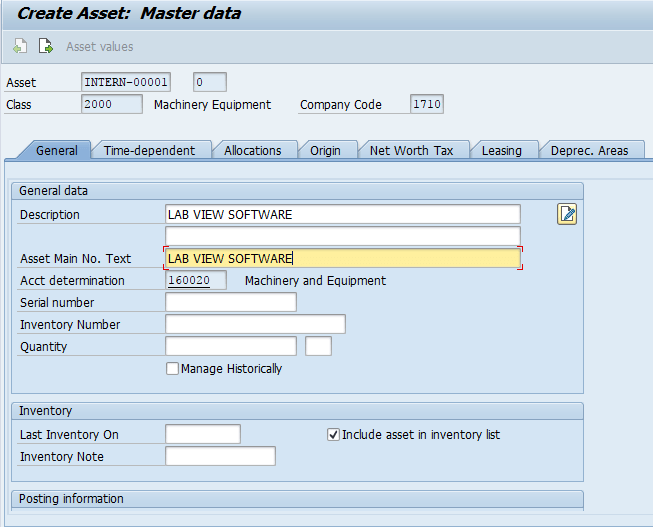

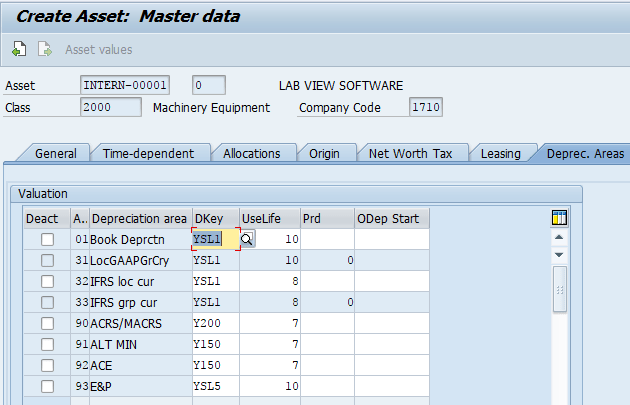

1.1 Create Assets – Asset under construction

1.2 Create Assets – for Final Settlement

We have created two asset master records, one Asset under Construction and one for the final settlement.

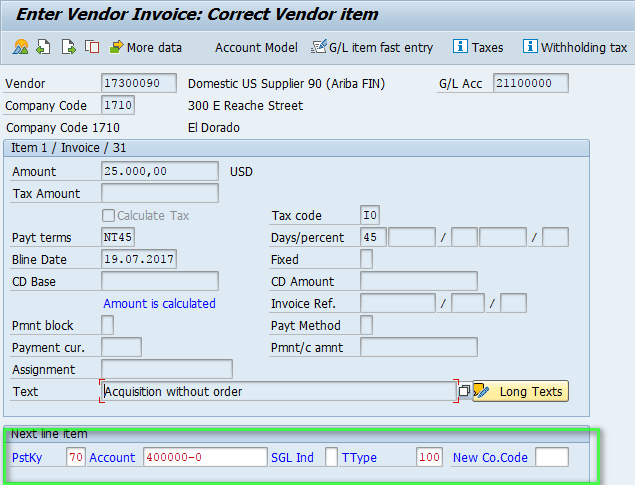

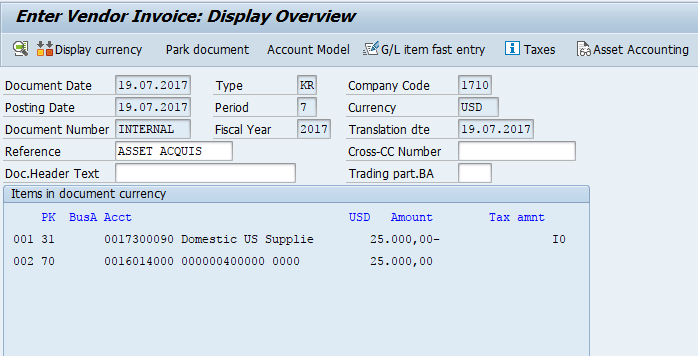

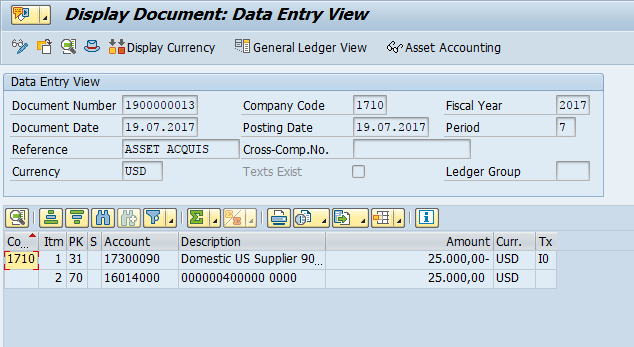

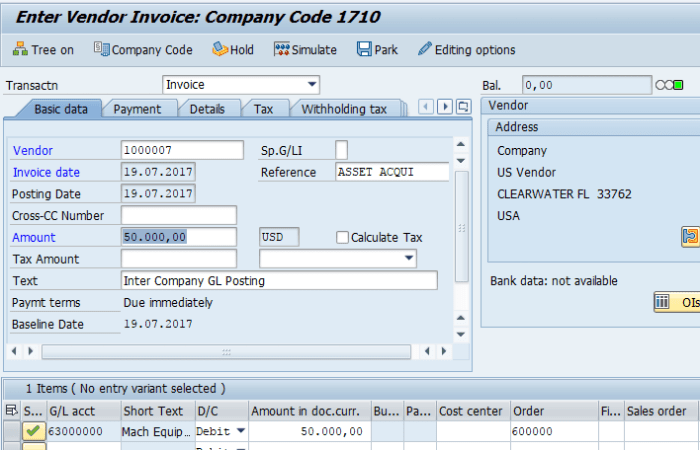

1. 3 Posting the Closing Invoice – Acquisition without order – FB01

In this step, you post the acquisition from purchase with vendor.

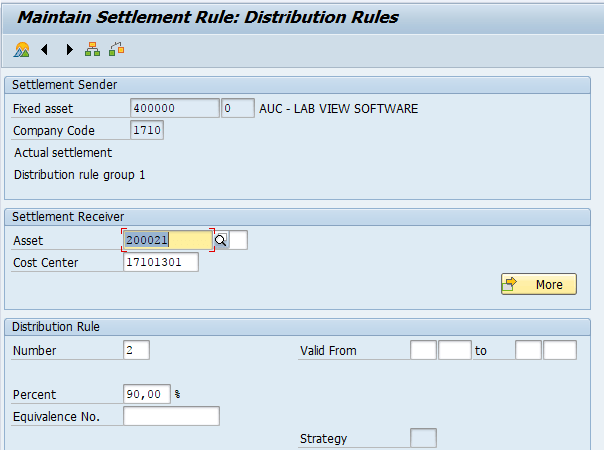

1.4 Define Distribution Rules for Asset Under Construction AIAB

In this process step, you maintain the settlement rules for the Asset under Construction created in the previous steps.

You have maintained the rules for the settlement. The execution of the settlement is part of the periodic processing.

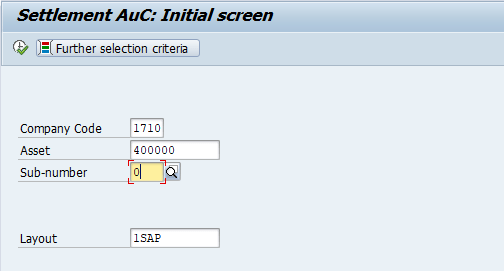

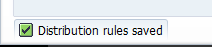

1.5 Settle Asset under Construction – AIBU

With the execution of this step, Assets under Construction are settled according to their settlement rules.

Note Under certain conditions, you may need to capitalize an asset under construction before all suppliers have presented their closing invoices. This can cause a few difficulties, especially if the closing invoice cannot be posted until the fiscal year following the capitalization of the asset under construction, and down payments were already posted to the asset under construction.

Initially, you post the down payment normally. If you then need to capitalize the asset under construction at the end of the fiscal year, but before the closing invoice is received, you post reserves for the total amount of the expected invoice. You post these reserves directly to the capitalized asset (external acquisition with vendor, transaction type 100). In the case where you plan to distribute the values from the asset under construction to several final assets, it makes sense to post the reserve to the asset under construction first, and then capitalize it. Whichever method you use, you must reverse the down payment on the asset under construction, because the down payment is not allowed to appear in the account for down payments to fixed assets. Instead, it must appear in the account for completed assets.

To settle the asset under construction, down payments must be cleared with invoice or forecasted invoice (reserve). The asset under construction can only be settled after this clearing

2.1 Asset Acquisition for Constructed Asset (Investment Orders /Internal Order)

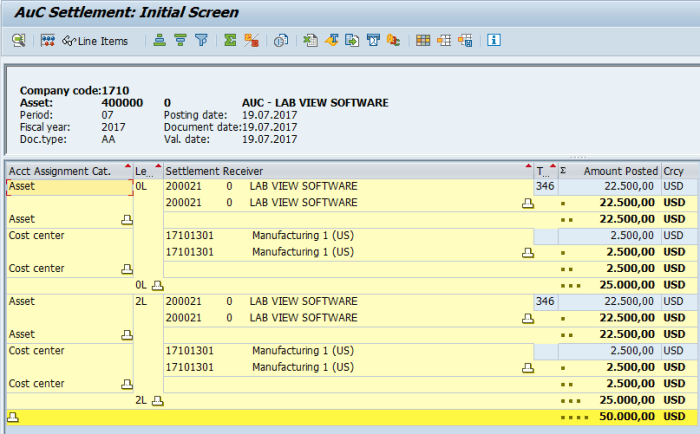

2.1 Create Internal Order – KO01

2.2 Release Investment Order / Internal Order – KO02

This activity releases investment order.

2.3 Accounts Payable – Posting Invoice to Investment Order – FB60

In this activity, you can enter a supplier invoice without reference to a purchase order.

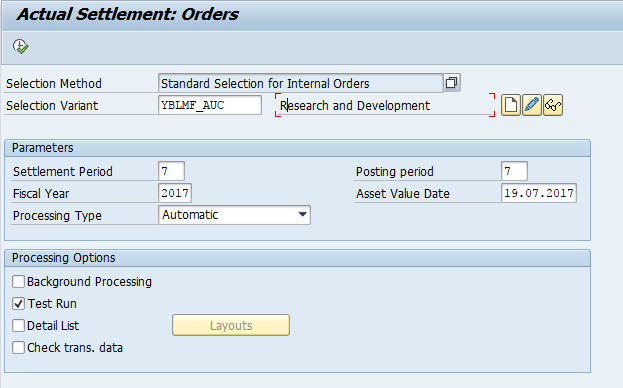

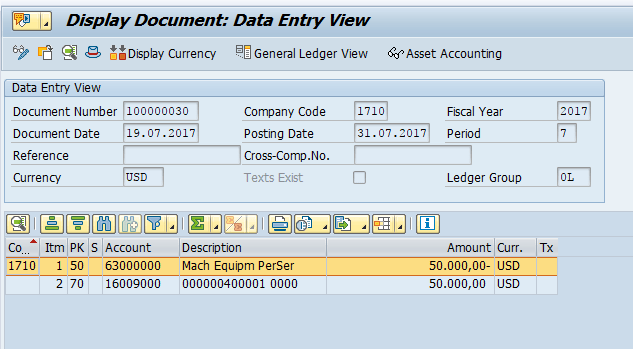

2.4 Asset under Construction Settlement – KO8G

In contrast to assessment, you cannot perform settlement across fiscal year boundaries. The system automatically determines the posting date from the posting period/fiscal year using the last day of the posting period. There are three processing types defined for settlement:

- Automatic: The system selects all the distribution rules for a sender.

- Periodic: All distribution rules with settlement types PER and AuC are selected. PER rules are applied first. In investment measures, this is followed by settlement to assets under construction.

- Partial capitalization: Use this processing type if you want to partially capitalize an investment measure which is not yet complete, that is, if you want to settle part of the overall cost to finished assets.

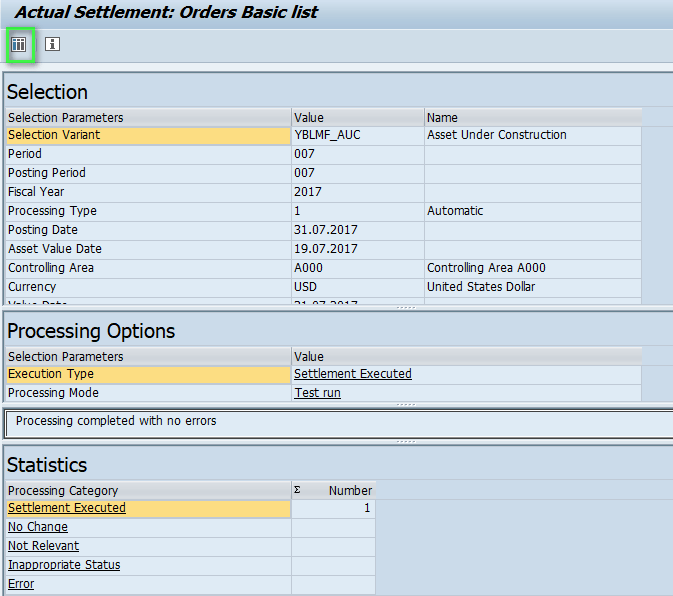

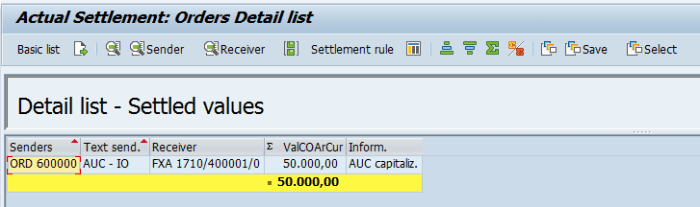

With this process step a periodic settlement is executed. All costs collected on the investment order will be settled to the automatically created AuC.

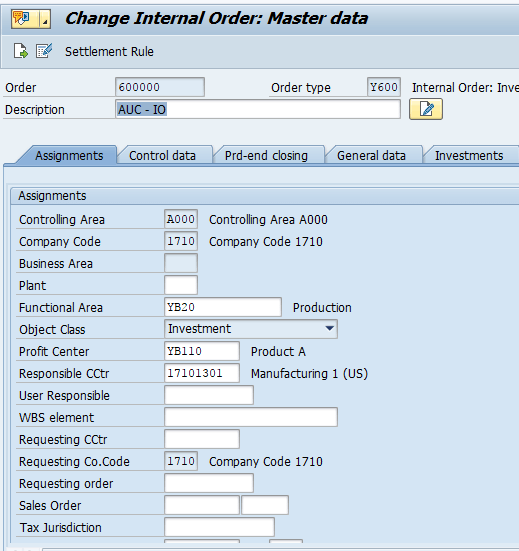

2.5 Create Internal order Settlement Rule – KO02

In this process step the settlement rules for the final settlement are maintained and the status of the investment order will be set to technical completed, which allows the final settlement of the order.

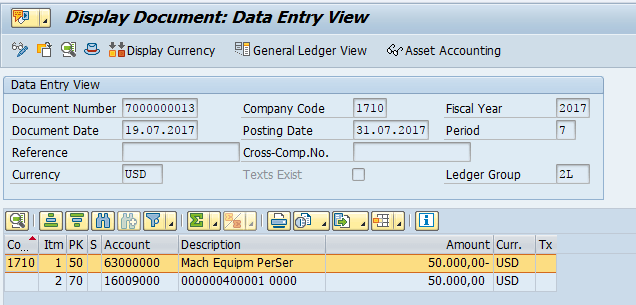

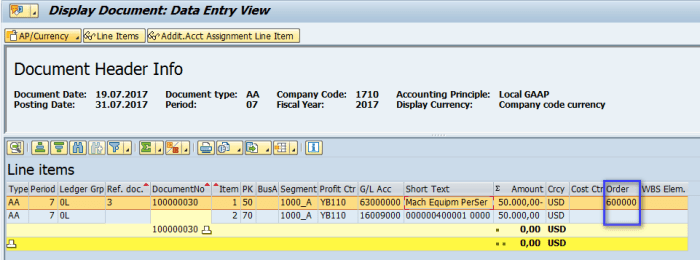

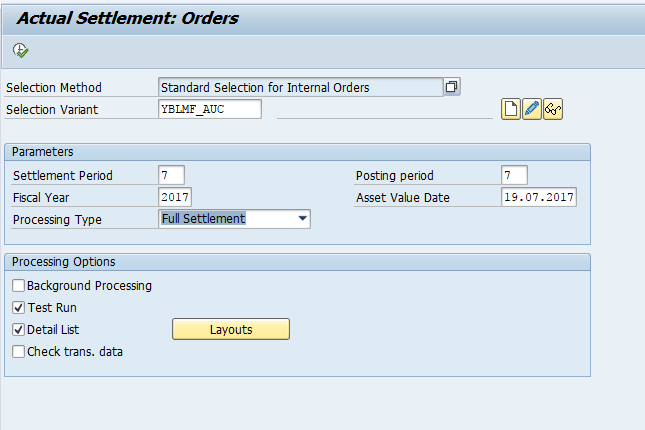

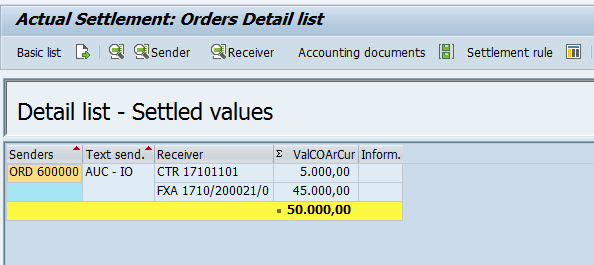

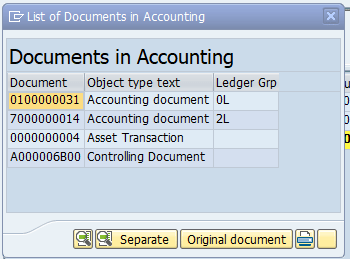

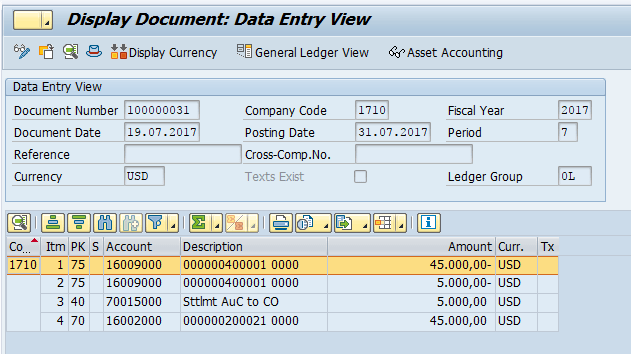

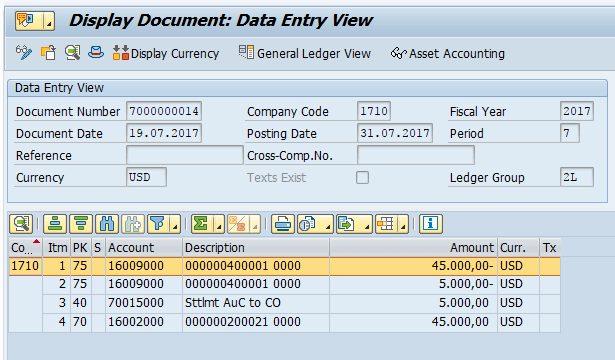

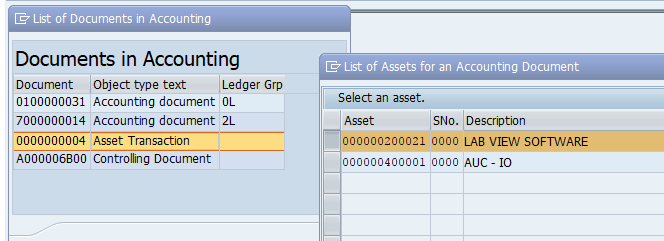

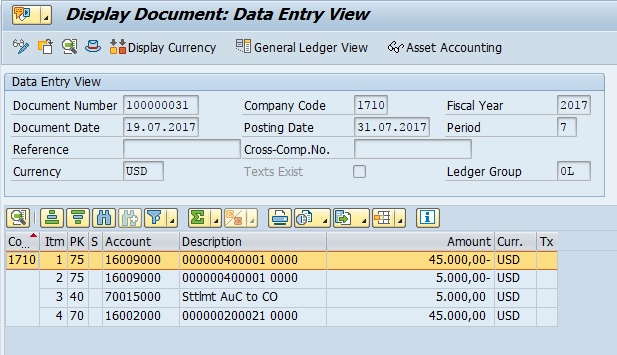

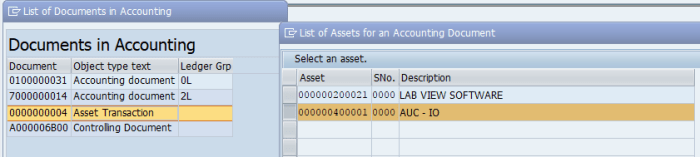

2.6 Final Settlement of the Investment Order (Collective Processing) – KO8G

The final settlement transfers the costs from the AuC asset to the completed asset and to the cost center as specified in the settlement rules. After the final settlement the balance of the investment order and of the AuC is zero.

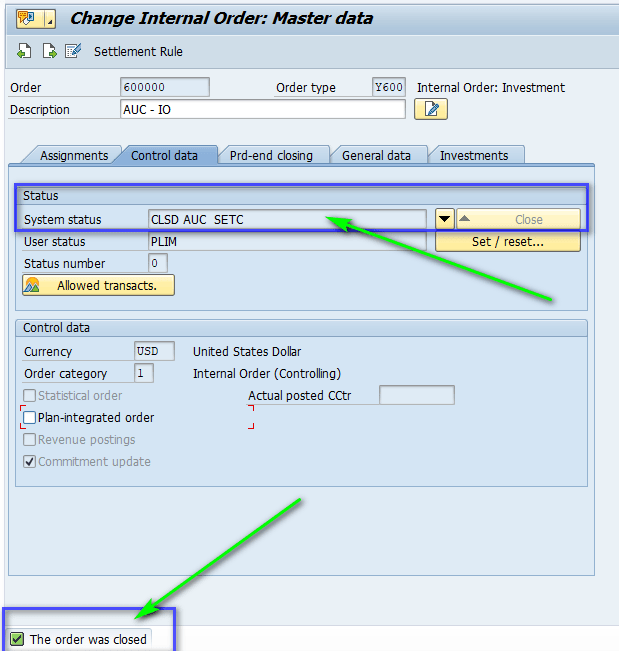

2.7 Completion of Investment Order -KO02

In this process step the investment order is closed by changing its status to Closed.

Thank You

Jayanth Maydipalle